Montgomery Investment Technology, Inc. has been providing Performance Price Target (PPT) valuation services to a wide range of corporations for over twenty-five years. The fair value calculations generated using Monte Carlo simulation are compliant with ASC 718 and IFRS 2.

An ASC 718 PPT valuation is a specialized financial appraisal required by U.S. GAAP (Accounting Standards Codification Topic 718) to determine the fair value of equity awards that vest based on a Performance Price Target.

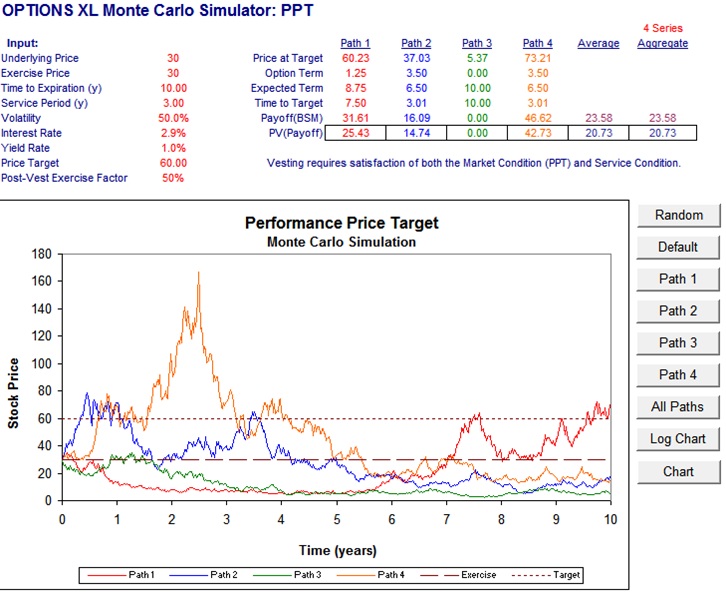

Because these awards depend on future stock price performance, they cannot be valued using simple formulas like Black-Scholes. Instead, they require complex “stochastic” modeling, typically Monte Carlo simulation.

An ASC 718 performance price target award is an equity incentive where vesting is tied to the company’s stock price reaching a specific level (e.g., the award vests only if the stock price hits $50).

In the world of financial accounting, ASC 718 distinguishes between performance condition and market condition awards.

1. The Critical Distinction: Market vs. Performance

Under ASC 718, a price target award is classified as a Market Condition, not a Performance Condition:

- Performance Conditions are internal metrics (revenue, EBITDA, EPS). If you miss these, the expense can be “reversed.”

- Market Conditions are external stock metrics (Stock Price, Total Shareholder Return). If you miss these, the company still has to report the expense.

2. How is the Fair Value Calculated?

Because a stock price target is “path-dependent” (the stock might hit $50 and then fall, or never hit it at all), you cannot use a simple Black-Scholes model. Instead, companies almost always use Monte Carlo simulation.

- The Simulation: specialized software runs 100,000+ “paths” for the stock price based on expected volatility and risk-free interest rates.

- The Probability Factor: The model calculates how often the price target is hit across all those paths.

- The Result: The “Fair Value” is essentially the average value of the award across all those scenarios, discounted back to the grant date. Because there is a chance the target is never hit, the Fair Value of a price target award is usually lower than the current stock price.

3. How is it Reported?

The reporting for these awards applies two unique rules:

- Fixed Expense: Once the Monte Carlo model sets the value on the grant date, that expense is locked in. Even if the stock price goes to zero and the award never vests, the company must continue to recognize the full expense on its income statement.

- Derived Service Period: Since there isn’t a “calendar” date for vesting, the Monte Carlo model predicts the “median” time it will take to hit the target (e.g., 2.4 years). This is called the Derived Service Period, and the company spreads the expense over that timeframe.

- Acceleration: If the stock price hits the target sooner than the model predicted, the company must immediately “catch up” and recognize all remaining expense at once.

The following resources provide insight into the depth and the services that MITI can deliver:

MITI White Paper – Performance Price Target Awards Basic Principles

Performance Price Target Working Paper

PPT Valuation Consulting Services

Sample PPT Valuation Report